From: https://www.davidstockmanscontracorner.com/once-upon-a-fomo/

Today’s Wall Street Journal features the highest paid CEO in America that you never heard of. And he runs a company called Paycom Software Inc, which you have probably never heard of either.

His name is Chad Richison of Oklahoma City and his pay was $211 million last year according to the company’s SEC filing and $711 million according to an alternative analysis performed by a reputable outfit called Institutional Shareholder Services. Either way, the man’s paycheck was equal to between 11,000 and 36,000 of the jobs wiped out in the leisure and hospitality sector last year.

To be sure, Mr. Richison deserves to be rich. He founded a company in 1998 which now serves over 26,500 small- to medium-sized business customers with human resources and payroll support.

The company’s full suite of products is cloud-based and delivered via the web and includes features such as talent acquisition, time and labor management, payroll processing, talent management and HR services. These activities generated $841 million of sales during 2020 and self-evidently provided stiff competition via some kind of better mousetrap to established incumbents like Automatic Data Processing and Workday.

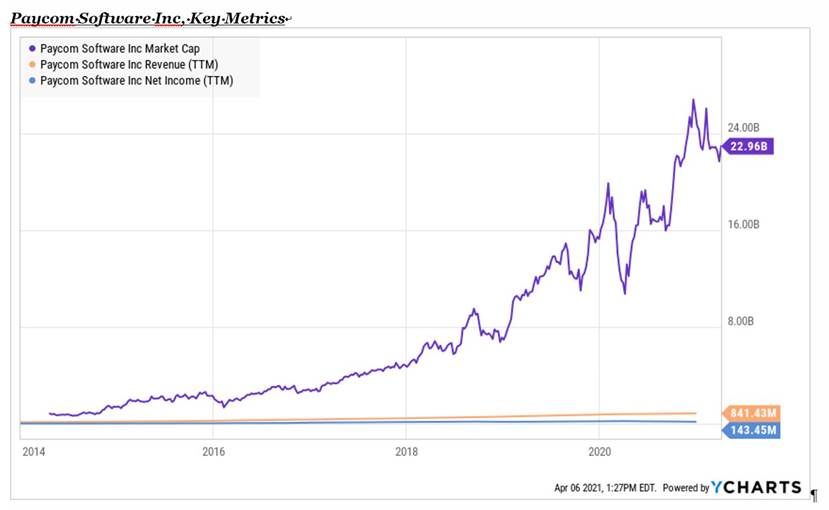

Then again, at its recent peak the company’s market cap stood at $26.7 billion, which is a cool 187X its 2020 net income of $143.5 million. So you would guess this company is some kind of rocket ship, with sales and net income arcing toward the moon.

Not exactly, however. The company’s 2020 net income represented just a 5.1% growth rate over the three years since 2017, when it posted earnings of $123.5 million.

Even more to the point, its operating free cash flow has been essentially stagnant during the past three years. Even then, the implied free cash flow valuation multiple has soared from an already frisky 65X to an out-of-this-world 201X

Operating Free Cash Flow and Valuation Multiple, Paycom Software Inc. 2018-2020:

- 2018: $124.8 million and 65X ;

- 2019: $131.4 million and 116X;

- 2020: $133.1 million and 201X.

In short, the free cash flow of this 22 year-old company has been growing at just 3.1% per annum. But that cash flow–which is the true metric for measuring a company’s economic rather than accounting profits—is being valued at 201X actual 2020 results!

Needless to say, that’s the skunk in the woodpile. Namely, a seemingly capable, innovative company offering a highly demanded services, but being valued at utterly absurd multiples of net income and free cash flow.

And it has actually gotten worse in recent years as the Fed has invented one new excuse after another to flood the market with liquidity and cheap debt, which has, in turn, fueled unprecedented Wall Street speculation and relentless financial engineering in the C-suites.

In the case of Paycom, the per annum growth rate over the past three years are as follows:

- Net income: +5.1%;

- Sales: +24.8%;

- Market cap: +71.6%

In turn, that’s what stock-based compensation in the Fed’s wildly inflated casino leads to. Namely, paychecks for top executives and Wall Street operators that are so grotesquely outsized that it is only a matter of time before voters grab their torches and pitchforks and demand an end to the farce.

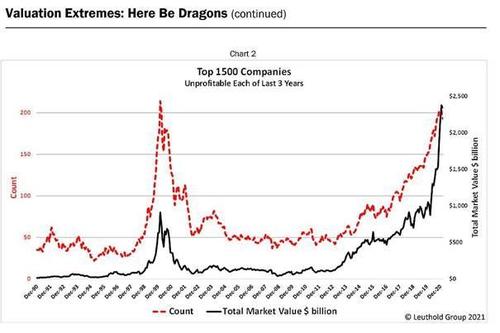

At least, Paycom is profitable and offers an on-line service that is being validated in the marketplace. By contrast, there are now 200 US companies out of the top 1500 publicly traded corporations which have been unprofitable for three years straight, yet collectively carry a market cap of $2.4 trillion.

That’s right. No profits for three years running and they are valued at $2.4 trillion with a “T”!

As shown below, both the number of loss-making companies and their combined market cap is now at the early 2000 peak. More importantly, these outlandish numbers compare to a normal trend where there are about 50 unprofitable companies with a combined market cap of less than $500 billion.

Jason Zweig summed up the current financial madness as well as possible:

“This isn’t a bull market or a bear market. It’s a know-nothing market.

Bragging rights used to go to those investors who worked the hardest at learning the most. Now the glory often goes to those who know the least and don’t even care.

‘I don’t know what the f— I’m doing,’a young man said in a TikTok video in January. ‘I just know I’m making money.’ He added that he’d been trading stocks for only three days, but ‘just like that, made $300 for the day.’ In the next few weeks that young man, Danny Tran, racked up roughly 500,000 followers on TikTok.”

“You could have made good money even with bad stock picks. It was like being invited to bet on black, without limits, at a roulette wheel on which 37 of the 38 pockets were black.

Why waste time and energy educating yourself while sheer ignorance pays off so easily?”

But here’s the thing. It’s not just this Tik Tok fan boy, the modern day equivalent of Joseph Kennedy’s famous shoeshine boy of 1929, who apparently has no clue about what he is doing.

Two of the most egregious financial blow-ups of recent weeks,

1. the Archegos fund and

2. Greensill Capital

left the likes of Credit Suisse drowning in upwards of $6 billion of losses. Yet in both cases, the level of speculative danger should have been plain as day to even the shoeshine boy.

In the case of Greensill, the earnings of the Credit Suisse sponsored funds were way, way too good to be true for the hum-drum business of trade financing. Likewise, in the case of hedge fund artist, Bill Hwang, Credit Suisse was essentially lending its own highly-leveraged balance sheet for modest fees from Archegos in what is called in the prime brokerage world of Wall Street total return swaps and contracts for differences.

The purpose of these fee-based arrangements, of course, is to hid the ball from regulators, competitors and the company’s own bankers. In this case, Credit Suisse and other Wall Street prime brokers bought tons of stock in behalf of Archegos and then levered it to the hilt. It than paid any net gain over a base level to Archegos in return for the fees.

Needless to say, in an honest free market, total return swaps would not even exist. They are not an investment strategy; they are a transaction-fee intensive device to hide leverage and the true owner of the assets.

No real investor could make money over any reasonable period of time from buying these high cost swaps because profitability depends upon a relentless rise in the stock averages. That and the Fed’s incessant put under the stock market, which usually prevents big margin calls and painful payment draw-downs from the gamblers like Huang who purchase them.

By contrast, in an honest two-way market, the cost of the fees would offset most or all of the net of the swap-holders’ daily gains and losses. That’s because there is no value-added in the swap—just the extraction of rents by Wall Street.

Likewise, honest Wall Street prime brokers—that is, those big enough to fail and unsubsidized by the Fed’s cheap financing and endless coddling— would see them for what they are. To wit, just another dangerous incarnation of the age old bull market game of picking up nickels in front of the proverbial steam-roller.

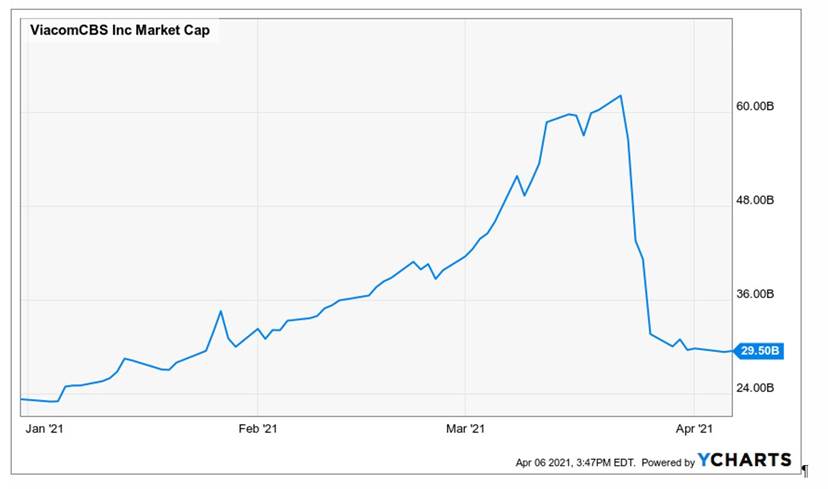

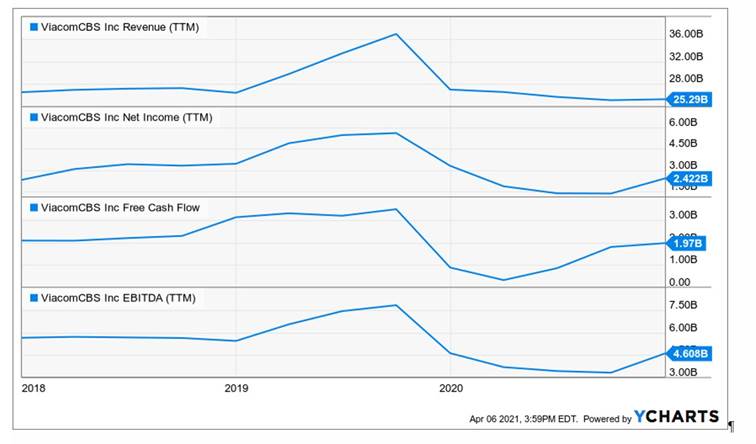

In the case of Archegos, speculator Bill Hwang added insult to injury by purchasing total return swaps on a very small number of companies from multiple prime brokers, thereby concentrating his bets in the most dangerous manner possible. Accordingly, the resulting heavy-buying by Wall Street in behalf of the Archegos swaps caused the price of dead-in-the water stocks like ViacomCBS to soar, which, in turn, attracted legions of homegamers and fast money Wall Streeters alike.

Accordingly, between January 1, 2021 and the peak of the frenzy on March 22, ViacomCBS’s market cap soared from $23.4 billion to $62.1 billion on no basis whatsoever except the favorite phrase in the casino: “Investors” were buying because the “price action” was spectacular.

Then again, there was nothing at all spectacular about the company’s financial performance that warranted any increase in its stock value at all.

In fact, for the year ending December 2020, here are the cumulative three-year changes since December 2017 for its key financial metrics:

- Net sales: -4.5%;

- Net income: +4.3%;

- Free cash flow: -5.3%;

- EBITDA: -18.4%.

Nonetheless, when Viacom announced an unexpected $3 billion stock sale to fund yet another Hollywood entrant to the streaming service (Paramount+), the stock hit the skids and Huang’s Wall Street prime brokers were left holding a plunging stock and a customer who refused or couldn’t meet suddenly massive margin calls.

Within a few days the Viacom stock was nearly back were it started the year, while Goldman Sachs and Morgan Stanley were crowing loudly that—after being suckered into the same trade—they had pulled the rip-chord with malice aforethought, leaving the hindmost of the losses to slower-footed brokers like Credit Suisse and the Japanese.

The larger point, however, is that the financial system is riddled with trillions of these kinds of central bank enabled wild-ass speculations. It is only a matter of time before the full-on dumpster fire on Wall Street begins to rage uncontrollably.

Still, as the WSJ noted Credit Suisse’s board is wont to treat these predictable fiascos as a one-off failure of risk management, just as Wall Street has done over and over since the giant meltdown of so-called “portfolio insurance” way back in October 1987.

In fact, however, these one-offs are endemic to a stock market which has been

1. transformed into a gambling casino by the Fed and which has seen

2. nearly every semblance of two-way trade and serious financial discipline destroyed by an ever-more supine and reckless central bank.

As the WSJ conceded, when you can profitably “buy the dips” for now 12 years running from the March 2009 low, it is not surprising that so-called risk controls fail again and again.

[ 20200119 Buy The Dip, An American Tradition Since 1987]

The investigations will also examine how the bank, after pouring huge amounts of investment into risk controls and oversight in recent years, allowed itself to get deeply involved in both situations. In the case of Greensill, the bank reviewed the relationship multiple times in recent years but continued to expand its business with the company.

But investors have been trained by the Federal Reserve to “buy the dips.” Importantly, even as valuations stretch suggesting lower future returns, investors continue to expect above-average results.

As the formidable Howard Marks observed in a recent Bloomberg interview, we have now actually reached the point where fear of losing money has been virtually extinguished. And he doesn’t hesitate to pin the tail exactly where it belongs.

“Fear of missing out has taken over from the fear of losing money. If people are risk-tolerant and afraid of being out of the market, they buy aggressively, in which case you can’t find any bargains. That’s where we are now. That’s what the Fed engineered by putting rates at zero.”

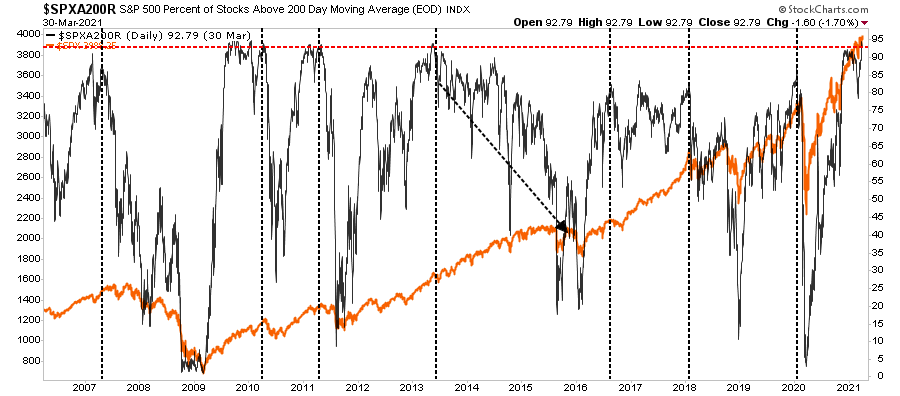

It should not be surprising, therefore, that 90% of S&P 500 stocks are trading above their 200 Day MA. [Day Moving Average] Ordinarily, that would be a flashing red cautionary warning about a stock market trading on fumes and ethers, but not in an environment where the main street economy suffered the Covid-Lockdown body blow last year, yet managed to gain 25% from the already sky-high January 2020 levels.

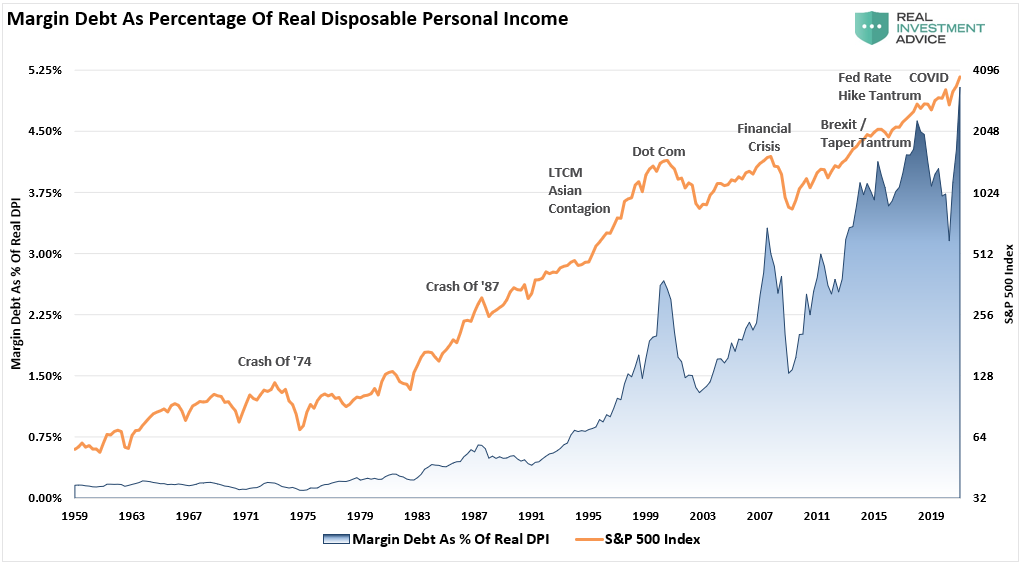

Likewise, margin debt has shot the moon. Measured as percent of real DPI, it now stands at an all-time record of 5.0%. That compares to

· just 3.3% at the 2007 pre-crisis peak and

· 2.6% at the dotcom top.

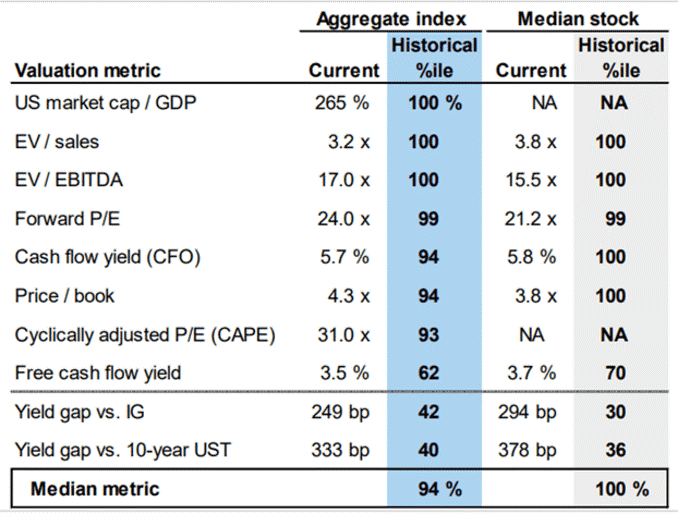

As it happens, even Goldman Sachs has let the cat out of the bag. As shown in the table below, stock prices in the aggregate are at the 94th percentile of history when averaged across a variety of metrics; and the median stock is actually at the 100th percentile.

Still, the fools in the Eccles Building insist that there are no speculative excesses in the financial markets. And they therefore assume license to keep money market rates at the zero bound and the bond market euthanized by $120 billion per month of supply removal in the guise of “accommodating” the recovery.

The longer this madness goes on, of course, the more violent and destructive will be the reckoning. And when that happens, as it already has four times in the last 34 years, the old saying will again be in force.

That is, when they raid the house of ill repute, the cops carry out the bad girls, the good girls and the piano player, too.

So

· Mr. Richison will loose much of his vastly over-valued fortune,

· the Robinhooders will be carried out on their shields and this time

· even Wall Street may be too far over the deep-end to rescue.

After all, the Archegos fiasco was not an outlier. Selling financial instruments of mass destruction is what the sum and substance of Wall Street’s hideously over-valued business is all about.